nj bait tax example

388000 50 of 800K less 24K of NJ BAIT deducted at entity level Federal Income Tax. This law was passed in response to the.

Nj Business Alternative Income Tax Bait Now Improved

After calculating the excess distributive income we multiply by the tax rate 109 and get 10900.

. 63087 10900 1100000 1000000 100000 x 109 10900 73987. Finally we add the 63087 base to the 10900 tax to obtain the elective entity tax. The 2020 New Jersey Business Alternative Income Tax may provide members.

S corporation S has net income of 1000000 in 2020 and one individual shareholder A. The entity must have at least one member who is liable for tax on their share of distributive proceeds pursuant to the New Jersey Gross Income Tax Act NJSA. Signed into law in January the BAIT is a new elective business tax regime in which New Jersey PTEs partnerships limited liability companies and S corporations can elect to pay an entity-level tax.

New Jersey joined the SALT workaround bandwagon this year by establishing its Business Alternative Income Tax BAIT. BAIT is a perfect example of a tax law that can only be taken advantage of with appropriate tax planning and staying in the know. Consider the following simplified example.

912 for distributive proceeds between 1000000 and 5000000. Single member limited liability companies and sole proprietorships may not elect to pay the Pass-Through Business Alternative Income Tax. Lets say that the partners share of the BAIT on New Jersey taxable income is 100000.

Each New Jersey resident members share of the entity level tax equals 565675050 2828375. 6308750 plus 912 percent for distributive proceeds between 1000000 and 5000000. Were going to take a deduction for the New Jersey BAIT paid in 1581750 resulting in 25918250 a federal income and allocated the three ways 8639417.

The New Jersey pass-through entity tax took effect Jan. Each member can use the BAIT credit to offset their member-level tax liabilities. 109 for distributive proceeds over 5000000.

The BAIT is intended to give New Jersey individual income taxpayers a work-around of the 10000 annual limitation on the deductibility of state taxes imposed by the federal Tax Cuts and Jobs Act TCJA commonly referred to as the SALT deduction cap. Tax is imposed on the sum of each members share of distributive proceeds which is 1500000. This new law allows pass-through businesses to pay income taxes at the entity level instead of the personal level.

5675 for distributive proceeds below 250000. For example if a retail business operating in New Jersey and applying the BAIT has two partners who were allocated 1000000 each then an electing partnership can pay the tax due on the owners share. Assume a PTE filed its 2021 BAIT return on March 1 2022.

The New Jersey Business Alternative Income Tax also referred to as BAIT or NJ BAIT helps business owners mitigate the negative impact of the federal state and local tax SALT. The PTEs distributive income is subject to tax at the following graduated rates for purposes of computing the BAIT. NJ BAIT Apportionment Factor For tax year 2021 S Corporations will have the option of using the single sales factor or the three-factor formula Sales Payroll Property to calculate NJ source income for resident and nonresident shareholders.

A partnership with a fiscal year of 1012193022 will file a 2021 PTE-100. By passing through a net amount of income reduced by the SALT deduction the owner is able to fully deduct their New Jersey taxes for federal purposes. Phil murphy signed legislation creating the business alternative income tax bait an elective entity-level tax on pass-through businesses for tax years beginning on or after jan.

Until 2022 there is a middle bracket of 912 for income between 1M and 5M. Business owners who fall into the qualified categories should reach out to their trusted advisor or accountant in order. The BAIT for New Jersey S Corporations continues to be limited to New Jersey-sourced income.

Changes are effective for tax years beginning on and after January 1 2022. Using the graduated tax schedule tax on 900000 would be 5656750. 6308750 45600 1500000-1000000 500000 x 912 45600.

54A1-1 et seq in a taxable year. Using a tax rate of 652 from the state-provided tax table the tax would be approximately 65000 for each partner. Using the table above tax is calculated on the 1500000 as follows.

419 revises the New Jersey elective pass-through entity business alternative income tax which was enacted in January 2020. The value of that deduction on the federal return assuming the maximum marginal rate of 37 is worth 37000 but the potential loss of the resident credit on the out-of-state partners tax return is the full 100000. Now if we apply the max rate in 2020 37 that will result in a tax of 31966 to each member.

652 for distributive proceeds between 250000 and 1000000. 1 effective immediately the legislation allows new jersey pass-through entities ptes to pay tax at the entity level and. For tax years beginning on or after January 1 2020 the four tiers of income tax rates are as follows.

5675 percent for distributive proceeds under 250000 1418750 plus 652 percent for distributive proceeds between 250000 and 1000000. Partners with a calendar year end of 123122 will claim credit for their share of the 2021 BAIT on their 2022 New Jersey tax returns. New Jersey has enacted the Pass-Through Business Alternative Tax Act BAIT.

Bracket Changes As a result of the amendments the BAIT increases to the top rate of 109 on firm income over 1M. 13 2020 new jersey gov. Income in excess of 1 million is taxed at 109.

Even if the IRS did take action through regulation or other guidance to disallow the federal PTE deduction for the NJ BAIT payments the partners members shareholders would still be allocated the state tax credit related to their allocable share of the NJ BAIT payment. Tax is imposed on the sum of each members share of distributive proceeds which is 900000. This act creates an election for pass-through entities PTEs to pay New Jersey income tax at the entity level and creates a corresponding individual income tax credit for the members of the PTEs.

140000 400K x 35 135800 388K x 40 NJ Income Tax. For 2022 you are required to use the 3-tier factor to calculate the NJ BAIT tax base. 24000 400K x 6 24000 400K x 6 The NJ BAIT tax deducted at entity level would be added back to taxable earnings for the calculation of NJ income tax.

Mechanics of the BAIT Election.

2

New Jersey Pass Through Business Alternative Income Tax Bait Updates Marcum Llp Accountants And Advisors

Tax Alert Faqs Released On Business Alternative Income Tax Bait Sax Llp Advisory Audit And Accounting

The New Jersey Business Alternative Income Tax Nj Bait What You Need To Know Rosenberg Chesnov

Teeth And Tax Season In 2022 Dental Dental Life Dental Costs

Nj Bait And New Salt Guidance What You Need To Know Smolin

New Jersey Pass Through Business Alternative Income Tax Act Bait L H Frishkoff Company

New Jersey Pass Through Business Alternative Income Tax New Jersey Mercadien

Dental Insurance 101 In 2022 Dental Insurance Plans Dental Insurance Dental Coverage

The Nj Pass Through Business Alternative Income Tax Act Alloy Silverstein

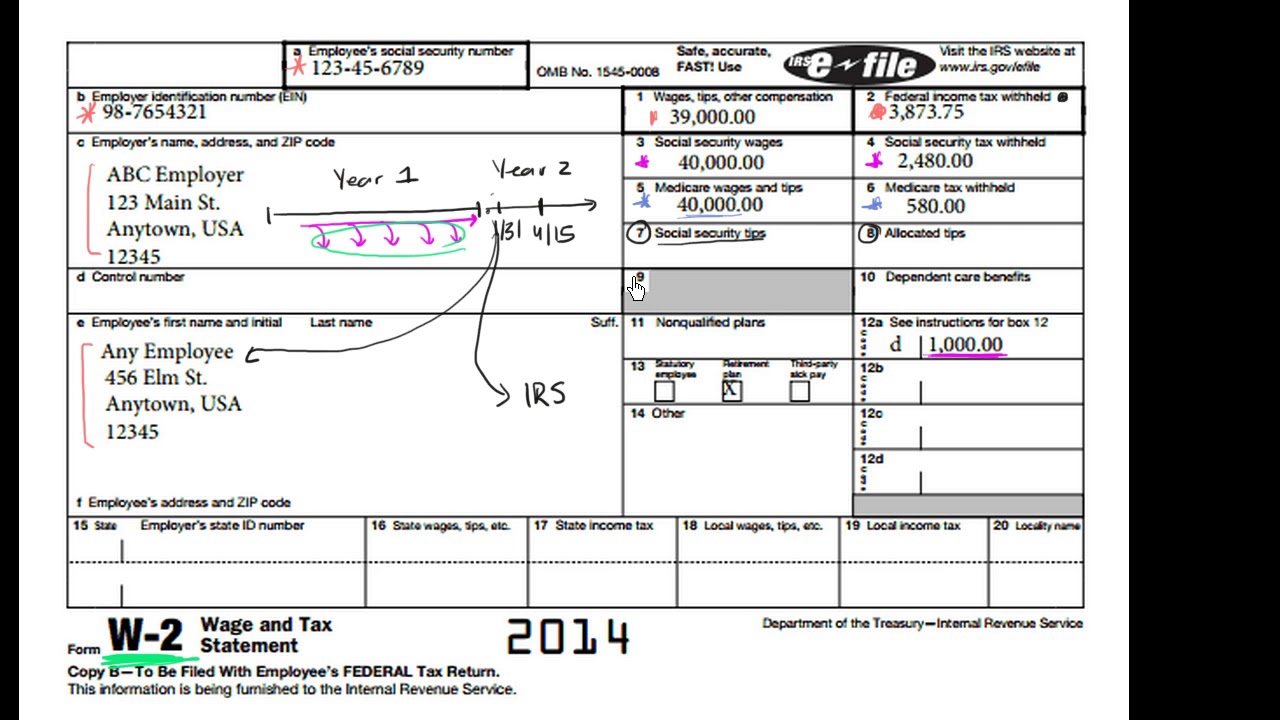

Intro To The W 2 Video Tax Forms Khan Academy

Irs Sweetens Tax Workaround For Nj Pass Through Owners Grassi Advisors Accountants

Nj Business Alternative Income Tax Bait By Michael Brown Cpa Prager Metis

Nj Pass Through Business Alternative Income Tax Professional Services

Intro To The W 2 Video Tax Forms Khan Academy

Nj Business Alternative Income Tax Bait By Michael Brown Cpa Prager Metis

Pass Through Entity Tax 101 Baker Tilly

New Jersey What Is My State Taxpayer Id And Pin Taxjar Support

Nj Bait Year End Tax Planning Considerations For Pass Through Entities Wilkinguttenplan